Why Is Temasek So Massively Overexposed to Chinese Regulatory and Market Risk?

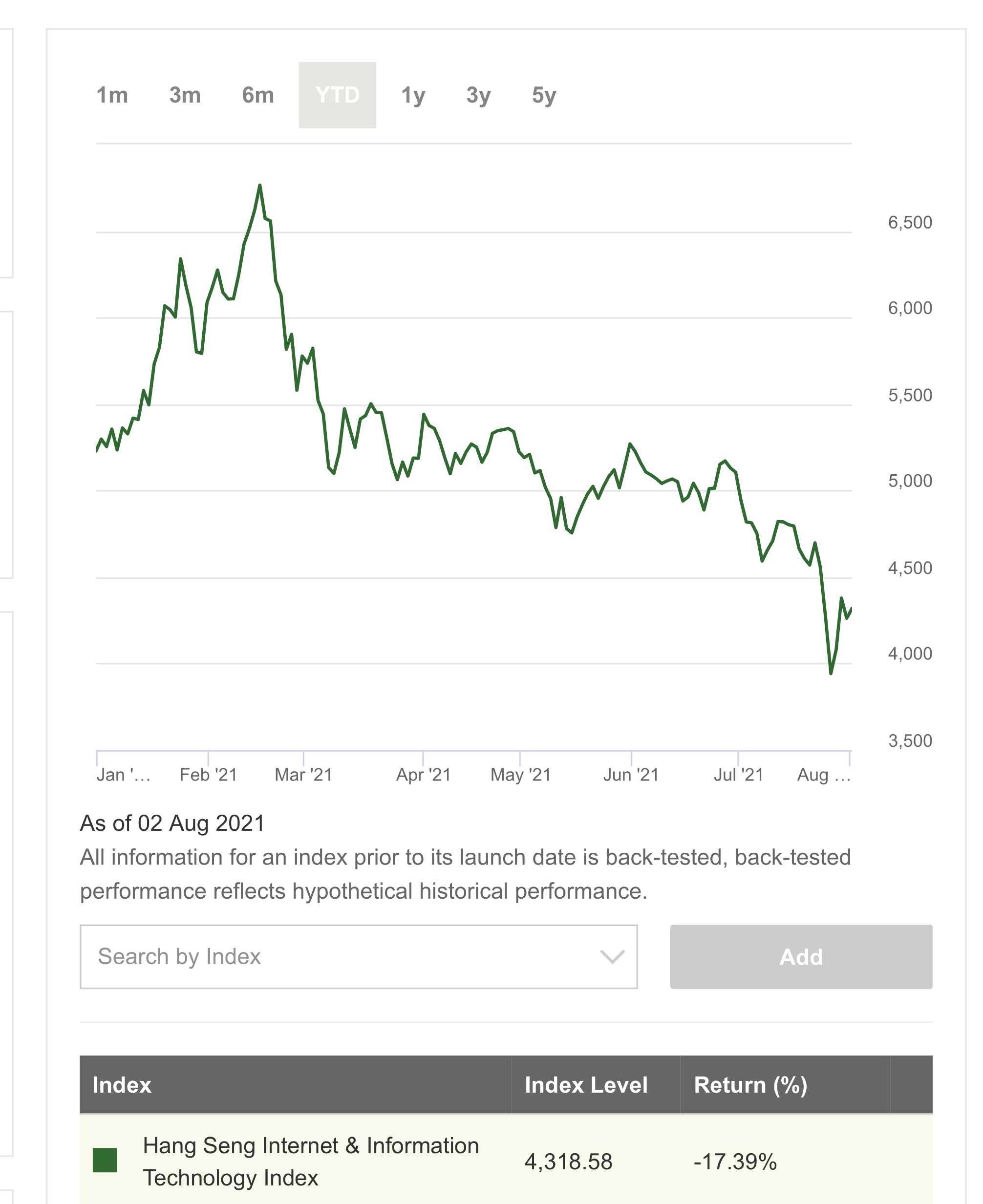

The last few days have seen a savage sell-off in Chinese tech stocks that has wiped hundreds of billions of dollars off their market capitalisation. The Hang Seng Technology Index has fallen some 24% since the date of Temasek’s year end valuation and by 43% from its peak. While there is no transparent market in pre-IPO and unlisted Chinese stocks the rout in these has been if anything greater. The last couple of days have seen the bubble bursting in the online education sector, in which, according to Bloomberg, both Temasek and GIC have been big investors. The Chinese authorities have issued new regulations barring for-profit companies and banning foreign capital from the sector, effectively wiping out their investment. As neither of our Sovereign Wealth Funds publish detailed breakdowns of their portfolios, it is impossible to know how much has been lost but it is sure to run into the billions.

The ostensible reasons for the Chinese crackdown on the tech sector are curbing monopoly power and the ability to discriminate against outside vendors in favour of their own companies and protecting consumers against fraud and misuse of their personal data. In the online education sector the reason given is to reduce pressure on parents to spend more on online tuition and thus indirectly boost the birth rate, a major priority for Chinese leaders.

Curbing the monopoly power of Big Tech strikes a chord with many Democrats and also Republicans in the US where curbing the dominance of big tech and its monopoly power is seen as a major priority and while the benefits to the consumer might prove elusive it is sold on the basis of promoting innovation. However in the US the Democratic administration has to contend with its small majority in Congress and the courts, where a Federal judge recently threw out an anti monopoly suit brought by several US states. Reining in big tech is a lot easier in China which has no rule of law and no real property rights. There is no requirement to seek democratic approval with the antitrust agencies functioning as investigator, prosecutor and judge rolled into one. However the real reason for the Chinese crackdown has more toCurbing the power of China’s tech billionaires is more about flattening all sources of potential opposition to Xi and ensuring that no new personality cults develop around people like Jack Ma that could threaten Xi’s rule.

The sell off in China is particularly ironic because just two weeks ago Temasek published its annual report accompanied by glowing articles in the state media and friendly (read sycophantic) foreign financial media like Bloomberg and the Financial Times with headlines like “Temasek posts best shareholder returns in 11 years.” Even without taking account of the sell-off since the balance sheet date, the historic 24.5% return in the year to 31 March 2021 is not as impressive as it appears when we remember that a year before that markets had fallen sharply at the beginning of the pandemic in March 2020. Then later in the year progress on developing vaccines and massive Government aid packages caused a gigantic relief rally. In fact between 31 March 2020 and 31 March 2021 the S&P 500 index rose twice as fast, by 53.7%, while the MSCI World Index rose by 52.0%. The Shanghai Composite Index only rose by 25% while the Hang Seng Technology Index.

Anyone who has read my blog knows that I have been scathing in my criticism of Temasek’s management, and in particular of Ho Ching for many years. (See links below to just a few of the articles). The precipitate plunge in the value of Chinese tech stocks reinforces all the doubts that Temasek’s management know what they are doing and in particular why they have put so many eggs in the Chinese basket. After all China only represents about 5% of global stock market capitalisation whereas the US represents over 55%. Temasek’s exposure to China is 27% of the portfolio whereas the whole of the Americas (North and South) is only 20%.

Being so overweight China carries huge political risk and makes Temasek hostage to a Communist Government that is no respecter of rule of law and does not care about foreign investors. On their website Temasek state that one strand of their strategy is betting on a growing middle class in Asia. If it is relying on China to fuel global growth then this strategy is already outdated since it has become clear that under Xi China is focused on becoming self-sufficient, presumably in preparation for conflict with the West. Consumption, and with it import growth have been downgraded which means less growth for the rest of the world unless the US tales up the slack (though to be fair both LHL and the PAP think consumption is an unnecessary evil like the Chinese leadership and that ordinary Singaporeans should consume as little as possible and produce and export as much as possible).

Since these trends have been clear for some time why has Temasek (and GIC along with the rest of the Singapore Government) put so many eggs in the Chinese basket. It probably stems from the PAP’s China-centric mentality, which started with LKY, and belief in China’s unshakeable rise to world dominance. That is the best interpretation. However there may be other more sinister reasons. As I said in my last blog, Why the Greedy Gullibility of Temasek’s General Counsel Should Ring Alarm Bells, if the top management of Temasek can so easily be taken in by a scam that should not have fooled an ordinary retiree, how can Singaporeans have faith that they know what they are doing. How can we be sure that Temasek’s whole portfolio is not full of rotten apples. Instead of giving Singaporeans facts, overpaid, unaccountable and arrogant expatriates like Mukul Chawla are wheeled out to repeat nursery mantras like “Our stance on China remains unchanged in our optimism”

Temasek is clearly not there to maximize returns on Singaporean-owned assets since it would have reduced its over exposure to China (and Singapore which is still nearly a quarter of its portfolio) and put more of its money into the US if that were the case. It started as an instrument of industrial policy to grow Singaporean state-owned companies but that rationale no longer exists since these companies no longer need state help and in fact are candidates for break up since they rely on monopolies and overcharging Singaporeans. Many of them, like DBS, have expat managers while others, like Keppel, Sembawang Marine and Singapore Airlines have workforces that are either largely or substantially foreign. In most cases Temasek owns only a minority stake though seems to exert a degree of control much greater than its They should be fully privatized. As a first step Temasek should be split in two, with a Singaporean arm and a foreign investment portfolio. Ultimately, as I have advocated many times in the past, Temasek and GIC should be owned directly by Singaporeans through the issue of shares which would be listed, This would provide transparency and accountability which seems sadly lacking at the moment.

Clearly the management of Temasek do not know what they are doing which is ironic because I do not know what they are doing either. The muddled strategy, which can be used to justify any investment, opacity and the management’s lack of accountability for mistakes suits LHL and his wife as it provides them with a vehicle for his wife and family to use to promote their interests. They can pay sycophants like its expatriate management and buy loyalty globally. It is also provides a route for LHL to channel state resources secretly without any credible oversight to himself and his wife since Ho Ching’s salary, likely to be in the tens if not hundreds of millions of dollars. Since LHL does not have to tell Singaporeans what assets he owns, Temasek’s clout as a large investor might provide profitable opportunities for him and his wife to invest on a favorable basis in unlisted companies together with Temasek. Singaporeans will not be told about the losses it has suffered in the rout in Chinese technology stocks. The only certainty is that Temasek’s existence provides little or no benefit to Singaporeans, It is high time that Temasek (and GIC) were made properly accountable to the people starting with the salaries and job performances of its top management and how much money Ho Ching has been paid and will still have invested at Temasek after she leaves in October.

![]()

answer back